That's a Mouthful

For most people, this is a really difficult and confusing strategy statement. What I am trying to explain expands on the principle that; money makes money when it moves and money ONLY makes money when it moves. So... if we have to keep our money moving to make money, putting our money in even faster motion must make us more money even faster.

Safe Money Growth

Most people, self included, have a hard time associating velocity, or any other reference to speed, when it comes to relating it to money... the two just don't seem to relate to each other. By the end of this article, not only should you understand it, but you should have a brand new perspective about the "velocity" of your money.

Hopefully it will inspire you to get thinking about all the ways that you can "velocitize" the growth of yours, without exposing it to any risk or taxes.

First Look

When I was first shown the money velocity slide, like the one above, I didn't really get it... until Jim, one of my mentors, put the slide into motion and explained it to me. It all starts with "access to money."*

Side Note:

I'm struggling with how to label "access to money." If you've been reading my ramblings, I'm sure that you've noticed this and I am all ears for any suggestions that you might have about what to call or label "access to money." For now I'm using; reserve, private reserve, pool of money, pool of wealth... not really loving any of these. I'm open to thoughts and suggestions.

10,000 Foot View

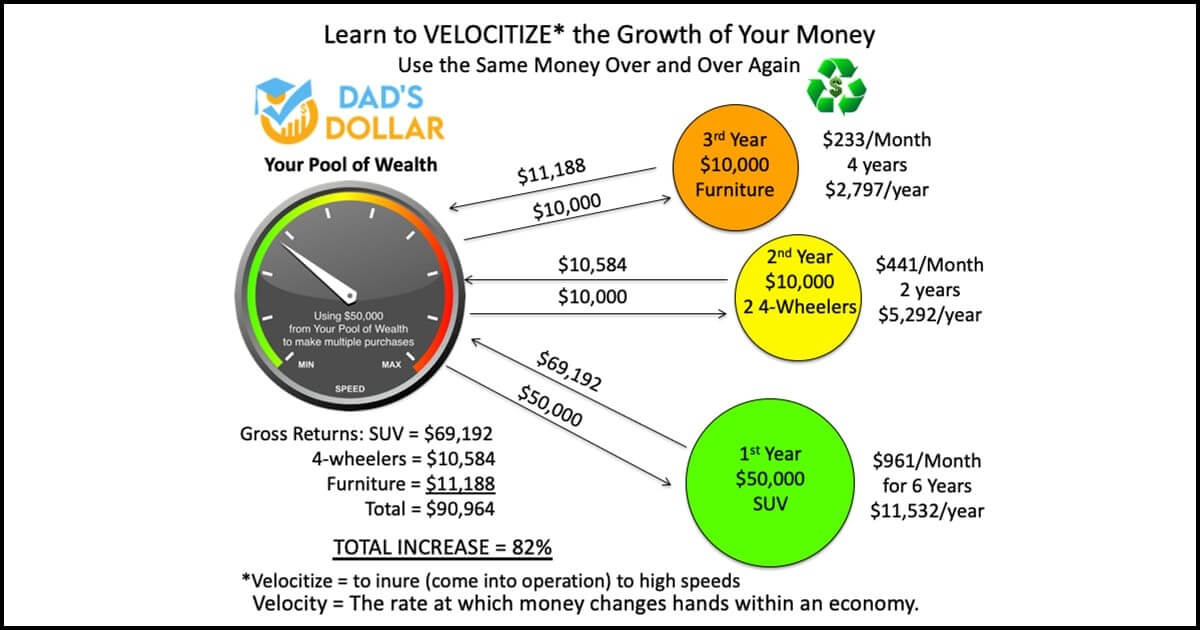

So on this slide, we begin with, and will only use $50,000. Take a zero or two off... or add a zero or two on... but please, please don't get stuck on the size of the numbers, instead, try to gain understanding of the principle. My mentors, who were pilots, used to always say; let's stay up at the 10,000 foot view rather than getting too low and getting tangled in the weeds. The weeds being the numbers and the math and the nitty-gritty.

This is a Critical Principle

“The very first principle that must be understood is that you finance everything you buy – you either pay interest to someone else or you give up the interest you could have earned otherwise.” Why not pay yourself the interest?

This Let's Break this Slide Down Step-By-Step:

- In the 1st year, $50,000 moves to the SUV dealership to pay for the SUV

- A loan is setup with monthly payments of $961 to move back

- In the 2nd year, $10,000 moves to the 4-wheelers dealer to pay for the 4-wheelers

- A loan is setup with monthly payments of $441 to move back

- In the 3rd year, $10,000 moves to the furniture store to pay for the furniture

- A loan is setup with monthly payments of $233 to move back

What Is Happening

After a few years, let's see what's going on:

- There was $50,000 in the "Pool of Wealth"

- Three times money was borrowed, each time a loan was setup, three loans total

- After the three loans were paid back, there was over $90,000 back in the "pool"

- All the principle and all the interest was back in the "pool"

- The $50,000 was increased to $90,964 - about 82% growth

- This money was never exposed to any risk

- This money was never exposed to any taxation

Slide in Motion aka Video

A section of a video, aka putting the slide in motion, that might help to explain this better...

The Lesson

What was learned from this experience:

- This is exactly what the banks were doing to Eileen and I... or was it what Eileen and I allowed to happen to us because of our lack of *Specialized Knowledge?

- *Specialized Knowledge - How you access and where this "Pool" resides, makes all the difference in who gets richer from it!

- Instead of the "Pool of Wealth" residing at the bank, where all these loans were making the banker richer, the "Pool of Wealth" could be residing:

- Better > In a shoe box, under my bed, making just me richer

- Best > In an over-funded participating whole life insurance policy, at a mutual insurance company, making me, my family, and my next generations really richer

- The more loans that are structured from a pool of wealth, the more money moves and the more money is accumulated in the pool of wealth.

- Moving money could be considered money moving with a certain amount of speed... or velocity. Making money move faster is called velocitizing the money that is already moving which makes it increase in value, grow faster.

- Staying in control of and knowing what to do with our money, to keep using it over and over and over again, keeps us from having to pay someone else to use their money.

Important:

The very first principle that must be understood is that you finance everything you buy – you either pay interest to someone else (most people understand this) or you give up the interest you could have earned otherwise (most people do NOT understand nor do they ever account for this!).

Account For:

"... you give up the interest you could have earned otherwise" is called Lost Opportunity Cost and must be accounted for!

- You can witness lost opportunity cost not being accounted for from who I call the "I pay cash" people. These are the people that are so close to be able to really 'velocitize' their money and create some amazing wealth... but they chose to not educate themselves about this, or just didn't even know that anything like this could even be done (like Eileen and I).

- Not applying a value for Lost Opportunity Cost radically skews what the "I pay cash" people think they are saving by paying cash!

- Lost Opportunity Cost can be calculated by; <the amount of money> times <the annual growth of that money (had you kept it)> times <the total amount of time you would keep it>.

- In reference to the above slide; if we paid $50,000 cash for the SUV and didn't set up any loans, we would not have grown that pool to $90,964. The Lost Opportunity Cost would have been $40,964. This must be calculated when someone opts to pay cash!

- You can witness lost opportunity cost not being accounted for from who I call the "I pay cash" people. These are the people that are so close to be able to really 'velocitize' their money and create some amazing wealth... but they chose to not educate themselves about this, or just didn't even know that anything like this could even be done (like Eileen and I).

- Not applying a value for Lost Opportunity Cost radically skews what the "I pay cash" people think they are saving by paying cash!

- Lost Opportunity Cost can be calculated by; <the amount of money> times <the annual growth of that money (had you kept it)> times <the total amount of time you would keep it>.

- In reference to the above slide; if we paid $50,000 cash for the SUV and didn't set up any loans, we would not have grown that pool to $90,964. The Lost Opportunity Cost would have been $40,964. This must be calculated when someone opts to pay cash!

- You can witness this from what I call the "I pay cash" people. These are the people that are so close to be able to really velocitize their money and create some amazing wealth... but they chose to not educate themselves about this, or just didn't even know that anything like this could even be done (like Eileen and I).

- Not applying a value for Lost Opportunity Cost radically skews what the "I pay cash" people think they are saving by paying cash!

- You can witness this from what I call the "I pay cash" people. These are the people that are so close to be able to really velocitize their money and create some amazing wealth... but they chose to not educate themselves about this, or just didn't even know that anything like this could even be done (like Eileen and I).

- Not applying a value for Lost Opportunity Cost radically skews what the "I pay cash" people think they are saving by paying cash!

- Lost Opportunity Cost can be calculated by; <the amount of money> times <the annual growth of that money (had you kept it)> times <the total amount of time you would keep it>.

- In reference to the above slide; if we paid $50,000 cash for the SUV and didn't set up any loans, we would not have grown that pool to $90,964. The Lost Opportunity Cost would have been $40,964. This must be calculated when someone opts to pay cash!

What's The Point?

This was another one of my huge epiphany moments, studying this slide with my mentors. As I began to realize the pattern of accessing money from the bank and then see the horrendous volume of my money that was moving to the bank, simply because I didn't know of any other way to access money, I became infuriated, and then intrigued, and then motivated, to create my own pool of wealth and become my own banker.

After creating my own pool of wealth, and then deciding to help others to create their own pools of wealth, the biggest problem I continually witness is the lack of discipline to pay money back.

Not paying this money back creates another financial liability... more debt, which completely negates the reason for structuring our pool of wealth and trying to get our money moving.

I struggle with trying to understand why some people respect the bankers money more than they respect their own money, meaning that they would never think of not paying the banker back but not paying themselves back, and creating an even worse financial environment for them and their family, is perfectly acceptable to them?

Safe money growth is simply owning your own debt and making the payments to your "pool". 'Velocitizing' how fast your money grows simply means to create more debt that you own, even buying your debt back from the bank or credit card, and keep making the payments to your pool!

Leveraging your money, making your money do multiple things, rather than letting the banker leverage your money, is one of the smartest things you can learn to do with your money.

Hopefully this gives you a better understanding of the velocity slide and this gives you a better understanding of why it is so important to stay in control of your own money, use it to safely grow your wealth, your family's wealth and your future generations wealth.

For Your Best,

Dad